If you order too much inventory, you’ll spend more money than is necessary and end up tying up your cash. Cash is the lifeblood of a business, and ensuring that you have enough of it at any given time is important. Plus, excess stock might not be sold before the end of its shelf life, or it could become obsolete, which would make the purchase a complete loss.

On the other hand, if you order too little of an item and it sells out, then you’re missing out on potential sales and revenue. You also run the risk of upsetting your customers because they’re coming to you and expecting a consistent stream of products and services.

While an inventory shortage or surplus is almost inevitable for any business, it’s the businesses that can best balance the supply and demand equation that thrive. The good news is that there are a lot of resources and software on the market today that can make inventory management much easier.

With the advice in this guide and a little bit of practice, you’ll learn to order the right amount of stock for your business and keep your customers happy.

What is inventory management?

Put simply, inventory management is a systematic approach to sourcing, storing, and selling inventory. Inventory management, however, is more than just a straightforward tally of stock.

A well-managed inventory system lets your business make the most of its storage spaces, better serve customers by having the stock they want (when they want it), and save money by reducing costs and losses due to spoilage and theft.

Conversely, without an effective system of inventory management, businesses inadvertently hold on to inventory longer than needed, which is expensive and can be a potential liability.

Effective inventory management can be extremely useful, providing insight into key aspects of your business, including your financial standing, customer behavior, product and business opportunities, and even future trends. This makes it a valuable aspect of business in which to invest time and effort.

How to manage your inventory

The first and most obvious step in getting control of your inventory is documentation. You need a single place where you can keep track of all your purchase orders (stock coming in) and your sales orders (stock going out). When you’re just starting out you might be tempted to use pen and paper to keep tabs on your inventory. You might think this keeps things nice and simple, but this method has some notable limitations.

Pen and paper are hard to change without things getting messy. If your business is active, those stock levels are going to change a lot as you buy and sell more items. Paper is analog so it has no backups and isn’t accessible from multiple locations. As your business grows and more people need to see the stock levels, having everyone standing around a single paper ledge can get crowded fast.

Using digital tools

After struggling with these limitations, many new business owners will graduate to digitizing their inventory in the form of digital spreadsheets. Not only are these files great for crunching numbers, but they can be backed up for security and worked on by several people at one time (if you use cloud-enabled software). You can set up your own system for tracking your inventory and sales in the program, or you can use pre-existing inventory templates that help get things organized.

Yet the biggest drawback to using digital spreadsheets to update inventory is that they aren’t linked to the other operational parts of your business. As soon as you ship something out, the spreadsheet needs to be loaded up and updated. The same goes for when you receive a purchase order and need to add those items to your inventory. It’s a very manual process, even though it’s digital. While it’s a great start, the chance of errors with manually updating spreadsheets makes it hard to master inventory control. So what’s the alternative?

Inventory software can help you run the entire operations side of your business. Think of software such as inFlow as your business operating system. When you need stock in, you create a purchase order. When you need to sell something, you create a sales order. The best part is, as these documents are processed, your inventory is updated automatically.

Of course, there are other advanced features available too, such as barcoding, inventory sub-locations, serial numbers, and more (none of which is available in accounting-focused software like QuickBooks).

What’s more, good inventory software offers to do some of the thinking for you. After you set reorder points, inFlow can tell you when your stock is running low and that you should create a purchase order to make more. Let’s see a spreadsheet do that. There’s also reporting built right in to make it easy to do your accounting when tax season rolls around.

How to select the right inventory management system

While the specific type of inventory your business deals with may vary greatly depending on whether your business is focused on wholesale, retail, or manufacturing, the fundamental principles of how you manage that inventory are universal.

If we think of inventory as money, taking control of your inventory and maximizing what you have (while minimizing inventory — aka money — waste) is key. This means finding ways to reliably get an accurate picture of your stock.

To create greater visibility of stock levels, an effective inventory management system should leverage factors like:

You’ll also want to assess the type of inventory management system you use, as this can impact how well you see your inventory.

What’s the difference between periodic and perpetual inventory systems?

To better understand how well your inventory system is serving your business, let’s look at two key approaches to managing your inventory: periodic and perpetual inventory systems.

Periodic inventory system

As a more traditional approach to inventory management, a periodic inventory system depends on counting inventory at the end of a regular accounting period (such as every week, month, quarter, or even every year, depending on the business).

The key advantage of a periodic inventory system is that it’s relatively straightforward. The drawbacks of this approach, however, are that you have less real-time visibility of your inventory (depending on your accounting interval, you may go weeks, months, or more without a complete and accurate inventory count), and reorder point forecasting is challenging.

In terms of the visibility of your stock, we can think of a periodic inventory system as a snapshot — it shows you what you have at a certain fixed moment in time.

Perpetual inventory system

A perpetual inventory system tracks inventory, as the name suggests, perpetually. With this system, you record each instance of inventory movement, like purchases, sales, or transfers of inventory.

The key advantage of a perpetual inventory system is that a business then always has a clear view of its current inventory. This means you can make real-time inventory adjustments as needed, generating:

- Lower costs;

- Easier forecasting and reordering;

- Optimized fulfillment;

- Better customer service and customer retention (for example, by avoiding stockouts);

- Reduced inventory loss (due to factors like theft and spoilage).

In terms of visibility of your stock, a perpetual inventory system serves more as a live feed — it shows you what you have on hand at any point in time. Pairing a perpetual system like inFlow with StockTrim gives you even smarter forecasts and automatic reorder suggestions.

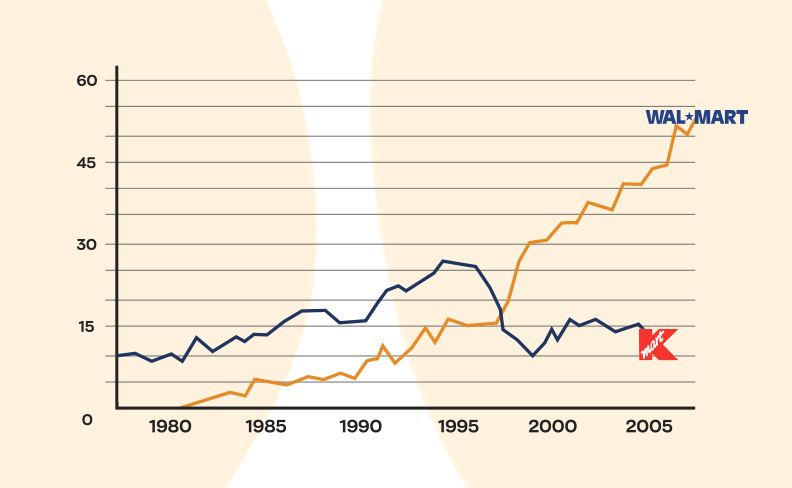

The impact of inventory in retail: Kmart vs. Walmart

To show the power of inventory management systems on business success, let’s turn to the striking example of Kmart and Walmart during their price war in the 1990s.

In the late ‘90s, Walmart implemented a new inventory management system that allowed it to restock its shelves more efficiently.

Its aptly named “just-in-time inventory” system cut down on excess inventory, which freed up cash that could then be invested into business growth. Additionally, this more efficient system provided better insight into customer needs — which made it possible for the company to offer more of the products that customers wanted at a lower cost and a lower price for customers. All in all, the increased efficiency of just-in-time inventory created a win-win situation for the company and its customers.

Alternatively, during the same time period, Kmart stuck with its traditional inventory management process.

The results speak for themselves: Between 1998 and 2000, Kmart stock prices dropped 63%, while Walmart stock prices rose by 82%. In the early 2000s, Kmart’s decline continued. The company filed for bankruptcy in 2002, closed hundreds of stores, and ultimately merged with Sears Roebuck in 2005.

By failing to adapt to new and more efficient inventory management systems, Kmart’s entire business suffered, while Walmart’s business thrived.

Ultimately, effective inventory management is a cornerstone of successful business operations. Embracing modern inventory management techniques and technologies ensures businesses maintain a competitive edge, streamlining their operations and facilitating smarter decision-making — all while benefiting profitability and setting you up for long-term success.

Where can I learn Inflow inventory full course?

Hi Venance, we don’t have a single full course for our products because they can be used in so many different ways. However, I think our inFlow Academy video series is a great place to start: https://www.youtube.com/playlist?list=PLZPdD9vxalF-zs9CUj8tvg3FKm-cT0hv7

After that, you can also check out our support page for more specific feature questions: support.inflowinventory.com

Cheers!

– Thomas